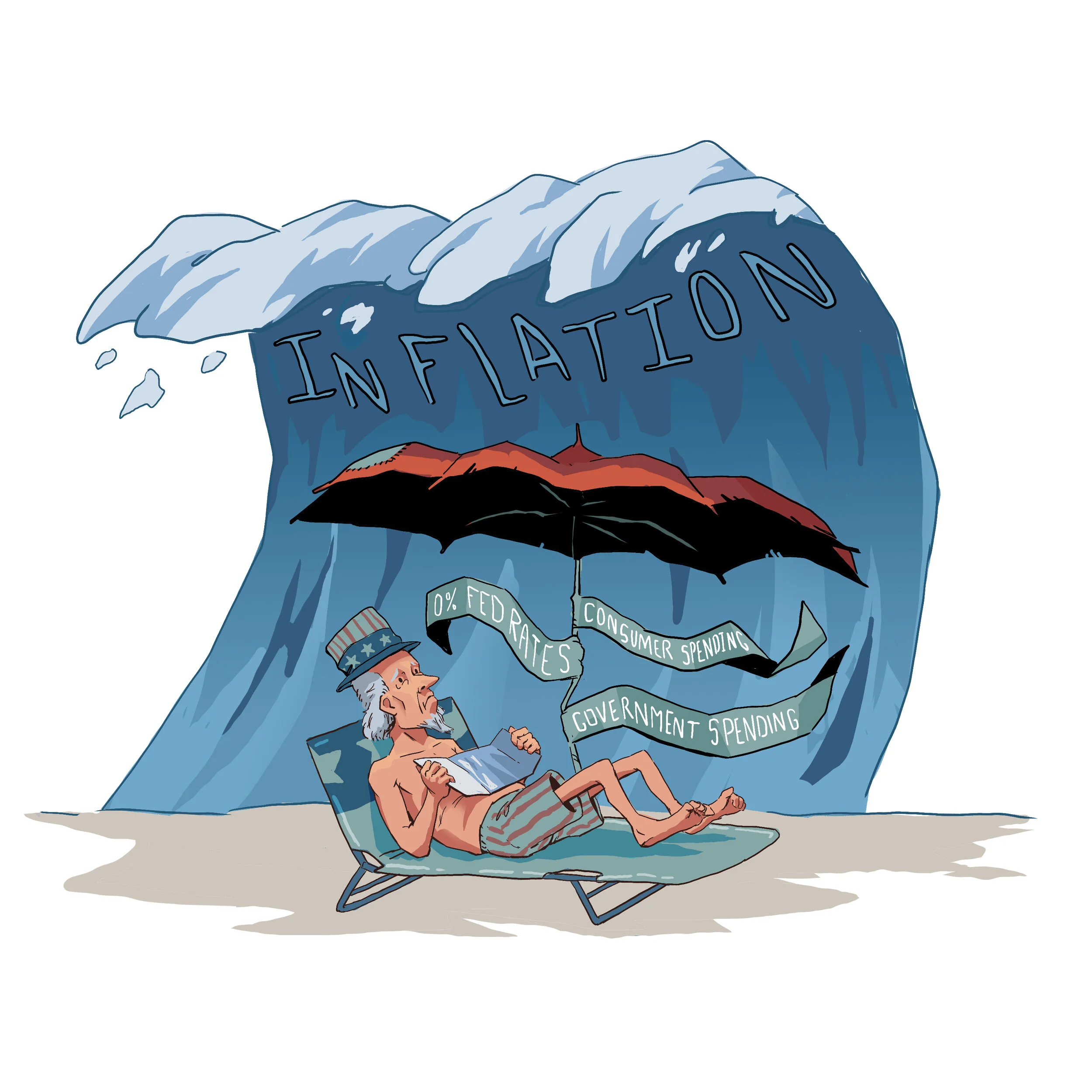

Wave Goodbye to Low, Low Prices?

Illustration by Thuan Pham

Are our Fears inflated?

What do you get when you fill a room with economists, and a passel of recess-deprived kindergarteners? Uncertainty? Chaos? Lines scribbled on the walls with intended meaning? Perhaps all of the above. Based on several significant indicators, the U.S. economy should be bracing for dramatically high inflation rates, but not all economists agree the result will be debilitating, or even notable. Let’s study some of the common rising price warning signs to help us determine if the nation’s predicted inflation surge line will soon be dramatically represented in permanent ink:

1. Cost-push inflation occurs when prices rise due to increases in production costs, such as raw materials and wages. Wages are typically the single biggest expense for businesses, and the trend in several states, and at the federal level, is to raise wages.

2. Natural disasters can also drive prices higher; the nation has suffered from dozens of these over the past decade. Should COVID-19 reside in this category?

3. Demand-Pull inflation can be caused by strong consumer demand for a product or service. One familiar example is the housing and business construction market, which is experiencing high demand for both new construction and renovating existing edifices. Building material costs for concrete, lumber, and steel continue to rise as manufacturing and distribution for those, and many other related items, are COVID-impacted.

4. Increased government spending on infrastructure projects are on the negotiation table, and Congress is facing pressure to deliver during this legislative session.

5. Rising Federal Reserve debt monetization (officially dubbed quantitative easing) is becoming monetary policy operandi; U.S. debt continues its precipitous climb as the Reserve buys U.S. Treasury bills, bonds, and notes from member banks, and recently, a diverse portfolio of corporate debt.

The Consumer Price Index, which measures prices for a shopping basket of goods and services, including food, cars, education, and recreation is predicted by many economic forecasters to exceed the persistent 2% inflation baseline targeted by the Federal Reserve Board, with several goods and services expected to rise well above that marker this year.

So which indicators are most predictive? What will the actual inflation rate look like for 2021 and beyond? Providing answers to those questions, and others, while interjecting relevant historical context, are our insightful native Wichitans, the Battling Bobs. Messieurs Litan and Love, who’ve provided unique perspectives over decades on the economic issues of the day, have graciously weighed in: which of their ideas pack the bigger punch?

Some Humility in Forecasting Inflation

By Robert Litan

Those of us, like the other Bob and I, who grew up in the 1950s and 1960s have seen lots of changes in our lives, in our society, our economy and our politics since then. But in the economic realm one of the most remarkable has been the taming of consumer price inflation.

Throughout the first quarter century of the post-War era, during which economic growth galloped ahead at almost an annual rate of 4 percent, compared to the anemic 2 percent over the past 15 years or so, a central concern of policy makers was how to reconcile low unemployment with low inflation. It was thought to be impossible, and indeed encoded into standard macroeconomic theory through the “Phillips’ curve” which traced an inverse relationship between the two: the higher the unemployment rate, the lower the inflation. The converse was true as well.

The Phillips curve relationship held up reasonably well until 1973, when the world literally changed: the oil embargo of the Arab OPEC nations quadrupled oil prices, which led to a lengthy period of “stagflation,” both high unemployment and high inflation. This continued after the Iranian revolution, which sent oil prices skyrocketing upward even higher. Only when the giant inflation fighter – literally – Paul Volcker became Fed Chairman in 1979 did the Fed turn off the monetary spigot, slowly squeezing inflation from its double digit heights of the late 1970s and early 1980s back into 4 percent territory by the time he was effectively forced out of his chairmanship in 1986 by dissenting Fed governors at that time.

But the inflation-fighting success came at a horrible cost, precisely what the Phillips Curve would have projected: a spike in the unemployment rate to a peak of nearly 11 percent in 1982, but it too began falling well into the 1990s and beyond.

In the meantime, of course, not everyone accepted the tradeoff between inflation and unemployment implied by the Phillips Curve. The most prominent critic was Chicago’s Milton Friedman who long championed the view that inflation was solely the product of printing money – “monetarism” -- and who later supplemented his views with a revision of the Phillips curve too. Friedman argued that low unemployment not only was associated with a higher rate of inflation, but that the inflation rate itself would accelerate over time, as firms and workers incorporated expectations of future inflation into their forecasts and began increasing their price and wage demands at an even faster clip. The only way to prevent this wage-price spiral was to nip it in the bud by cutting off monetary oxygen – namely, by strictly controlling the growth of the money supply.

Volcker adopted the language of monetarism to justify his inflation-fighting campaign – protesting (a bit too much) that all the Fed could do was control the money supply, and if interest rates soared in the process, which they did in the early 1980s, that was out of his hands. Of course, that wasn’t true, but Volcker’s public fealty to monetarism provided a convenient cover for fighting the inflation dragon without admitting that sky high interest rates helped him do that.

I recite all this history first to set the stage, but also to educate readers who may be a lot younger than the two “Bobs” of how inflation was so top of mind for much of the post-War period, at least until the 1990s, by which time it had fallen off to 4 percent or less, and since then has drifted even lower. Younger readers will therefore wonder, understandably, why inflation is such a big deal, since they’ve lived and grown up in a world of relatively low inflation by post-War standards.

Roll the clock forward to the decade after the 2008-09 financial crisis and the worst recession since the Depression. The government fought that event through a (then) unprecedented, and heavily disputed, combination of fiscal and monetary stimulus, which halted the recession and enabled the economy to recover over the next decade. Too slowly, as it turned out, since many economists (including yours truly) believe that the stimulus post -2008 wasn’t enough.

But whether it was or it wasn’t, throughout the ten years of post-2009 recovery, many monetarists kept warning that the creation of so much money, especially through Fed “quantitative easing” – large-scale purchases of government bonds, much of them with longer maturities – would eventually ignite a burst of large and continuing inflation. After all, Friedman had warned decades before that inflation was the product of “too much money chasing too few goods,” and so quantitative easing had to spark inflation.

But it didn’t, for a simple reason. Monetarism assumed that the “velocity of money” – the rate at which it turned over – was constant, so that the more money, the higher inflation. In the post-2009 world, however, velocity dropped and kept dropping, because so many people and firms kept the newly created money in their bank accounts and didn’t spend it, or if they did, they bought stocks and bonds, pumping up their prices, but not the prices of goods and services. As a result, consumer price inflation throughout the past decade has been remarkably subdued, at annual rates less than 2 percent, so low in fact, that Fed governors have wanted to push it a bit higher so they would have more room to cut interest rates in the future to fight off recession, and also to encourage consumers to buy more now, rather than wait.

Then the pandemic hit in March, 2020, sending the U.S. economy into a Depression-like tailspin. The Fed and the federal government responded with an even more unprecedented combination of money creation and government deficits from multiple “rescue” packages totaling about $5 trillion. And so now the inflation concern is back, this time with more than just monetarists worried. So, too, are leading Keynesians, like former Treasury Secretary Larry Summers and Harvard professor and former IMF Chief Economist Olivier Blanchard, formerly of MIT.

The current Fed Chairman, Jay Powell, is not as worried. Also in his camp is his predecessor and now the current Treasury Secretary Janet Yellen. The main reason they aren’t as concerned, aside from the persistent low velocity of money, is that 4 million workers have left the labor force since the pandemic, most of them women – indicating that there is a lot of slack in the labor market not captured by the 6% unemployment rate (which is computed by dividing the current numbers of unemployed seeking work by the total labor force, which includes the employed and those seeking work). With more slack, a bounce-bank in consumer demand should not lead to dramatically higher prices overall.

In addition, both Powell and Yellen, among others, point to the fact that if inflation picks up in a sustained way, they can fight it, as Volcker did, by constraining the growth of the money supply or raising short-term interest rates (by selling the Fed’s bonds and soaking up money that way). What neither Powell nor Yellen emphasize, however, is that if they are forced into raising rates, history says they are likely to spark another recession.

So, where does all this leave us? In a land of a lot of uncertainty, perhaps as much as any of us has seen in our lifetimes. Will the economic rebound, now widely forecast to show 6% growth in GDP this year, stall because the COVID variants get out of control and push the economy back down? Or will the variants be squashed by the vaccines, allowing a growth boom? If growth booms and causes supply shortages in parts of the economy – as would no doubt happen – will the price spikes be temporary, or will they set off a new economy-wide price-wage inflation spiral?

The truth is no one really knows the answers to these questions. My personal view is that given the quiescent nature of inflation for over a decade, it will take a sustained price jump across multiple sectors, perhaps over several months, to change market psychology. My bet is that this won’t happen.

But we could see a sustained jump in longer term interest rates – independent of what happens to inflation – or in “real” interest rates, if private sector investment rebounds and competes with the government’s heavy borrowing. For investors and homeowners that prospect to me is the most worrisome, though I can’t down a number for you, and most experts who have tried to do so in the past have missed. I don’t want to join that club.

The Inflation Psychosis

By Bob Love

Real money and civilization

"When the division of labour has been once thoroughly established, it is but a very small part of a man’s wants which the produce of his own labour can supply. ... In order to avoid the inconveniency of such a situation, every prudent man in every period of society... must naturally have endeavoured to manage his affairs in such a manner, as to have at all times by him, besides the peculiar produce of his own industry, a certain quantity of some one commodity or other, such as he imagined few people would be likely to refuse in exchange for the produce of their industry. … The use of metals [as the people’s common commodity] was attended with two very considerable inconveniencies; first with the trouble of weighing; and, secondly, with that of assaying them ... [which] gave occasion to the institution of coins, of which the stamp, covering entirely both sides of the piece and sometimes the edges too, was supposed to ascertain not only the fineness, but the weight of the metal. … It is in this manner that money has become in all civilized nations the universal instrument of commerce, by the intervention of which goods of all kinds are bought and sold, or exchanged for one another.”

― Wealth of Nations, Of the Origin and Use of Money, Book I, Chapter IV, Adam Smith, 1776

In a few short paragraphs, Adam Smith eloquently explains the virtue of real money in promoting the advance of human civilization consistent with natural order. I say “civilization” and “real” because at all times in Smith’s exposition, money is

a social medium functioning as a vital part of the people’s commonwealth [via their constitution]

derived from and attached to “real” commodities

meaning human economy remains safely restrained by natural ecology. [To understand why and how natural ecology comes before human economy see the e3 website and study the related links].

But, as sages from Moses’ 10 Commandments to Madison’s Federalist #10 and from Buddha’s Middle Way to Bastiat’s Law warn, humans rebel against nature’s restraints on their insatiable appetites … and so [what Keynes called] the “debauchment of the common currency” is inevitably conceived in the [what Madison called “improper or wicked”] minds of a few uncivilized delusionals … ie. elite sociopathic psychotics … and money is soon perverted for all and civilization set on a course to destruction.

Counterfeit-fiat money and psychosis

“Sociopaths are approximately 4 percent of the United States adult population. ... The chances that you will run into one are fairly high. It helps to recognize the patterns of their seductions and to always maintain a healthy skepticism, especially when your gut feelings sense something is contradictory about what a person says and what they actually do.”

― Will You Be Seduced by a Sociopath?, Psychology Today“Psychosis occurs when an individual [or group] loses touch with reality … [It] is a symptom, not a classifiable disorder in and of itself.”

― Psychosis, Psychology Today“When a delusional person’s bizarre beliefs spread to otherwise mentally healthy individuals via repeated contact with the abnormal person, the result is a shared psychotic disorder. The delusion contaminates others as if it were a contagion.”

― Is QAnon a Shared Psychotic Disorder?, Psychology Today

Roman emperors [except Diocletian] and American bankers [without exception] share a sociopathic lust for money. And both resort[ed] to the same practice to obtain more of it: put an official image on it to assure the public of its virtue then counterfeit it to deceive the public about its value … which begins with the physical adulteration of the coinage but ends in money’s complete detachment from any real commodity.

Hogeland’s Founding Finance explains how the American people’s common currency was hijacked by elite corporate and banking sociopaths [led by the adulterous Alexander Hamilton] before the Republic was even official.

Elder’s new thought provoking biography Calhoun: American Heretic tells how a few heroic second generation Americans realized that the common currency and public credit had been stolen by the elites and how they successfully restored both to the Republic as vital parts of the people’s constitutional commonwealth.

But Griffin’s The Creature from Jekyll Island: A Second Look at the Federal Reserve tells the story of Washington’s ultimate 1913 betrayal of the American Republic to the international corporate/banking cartel which rules the world today by controlling and manipulating its money.

After the Nixon Shock of 1971, the US$ [the world’s currency] became fully counterfeit, fiat money … with George Washington’s picture belying the Federal Reserve’s empty promise … as the US Treasury Silver Certificate was replaced by the Federal Reserve Note. But it gets worse.

Satan’s first miracle: turn debt into money … fiat credit

"Rather than seeking to liquidate the national debt, Alexander Hamilton recommended that government securities pay sufficient interest to be traded at par promoting their perpetual circulation as legal tender equivalent in face value to hard currency."

― First Report on the Public Credit, made by Alexander Hamilton to Congress, 1790, Wikipedia“As often is the case with addictions, the fanciful notion of a gradual discontinuance only provided a comforting pretext for more sustained indulgence.”

― Ron Chernow [on Alexander Hamilton's secret life of marital adultery]

With the US$ officially detached from real commodities in the Nixon Shock, the elite sociopaths were free to simply print infinite amounts of it for distribution to cronies. And that’s just what they did, until inflation raised its hydra heads [which modern science tells us neither age nor die] to threaten the existing social order ... as it inevitably does in the universally lurid and eventually disastrous history of paper money.

Fearing their monetary spell over the public might be broken by trying to answer lingering, unwanted questions about the prudence [much less the justice] of their practices, the elites selected an erstwhile Heracles named Volker to slay the unconstitutional fiat money creature they created to pillage the commonwealth and enslave the Republic.

But in the process they realized that they did not need to crudely print fiat money when they could subtly use the central bank to create fiat credit in non-repayable, unlimited amounts which could be distributed … at subsidized low interest rates … through the banking system … to credit-hungry public and private cronies … crushing the common currency as effectively as fiat money and crushing real savers as well while securing control of the broader market for public and private debt [and all other financial assets] … the Trojan horse that would permit them to enter the next phase of their global monetary mass psychosis and cement their central-planning control of the global economy.

Eating their offspring

“The exact evolutionary purpose of the practice by [certain species of eating their offspring] is unclear and there is no verifiable consensus among zoologists; it is agreed upon though that it may have, or may have had at some point in species' evolutionary history, certain evolutionary and ecological implications.”

― Wikipedia

Spawning unlimited public and private debt backstopped by central bank fiat credit quickly became the elites’ tactic of choice for plundering the world’s commonwealth … and remains so today. But they cannot stop with merely spawning debt that is inherently unpayable.

So, following Hamilton’s cunning act of rolling the colonies’ revolutionary war debts into the national debt to strengthen the powers of the central government and weaken state sovereignty, the global financial elites have conspired to dump the unpayable trillion$ of state, local and private debt they spawn into a sea of unlimited fiat credit by having central banks simply “buy the bad debt and bury the evidence of their adultery” in an act of filial cannibalism.

However, COVID interrupted/accelerated their plans … but since they cannot consume all the debt that is ready to collapse quickly enough, they have simply declared it suspended indefinitely in a desperate act of open totalitarianism … hopeful that the Republic’s short-sighted common poverty and mass monetary psychosis will maintain submissiveness.

Inflation: gospel or mirage?

“The art of economics consists in looking not merely at the immediate but at the longer effects of any act or policy; it consists in tracing the consequences of that policy not merely for one group but for all groups.”

― Economics in One Lesson, Chapter 1: The Lesson, Henry Hazlitt, 1946

The next act in this tragedy is for the elites to use their economist priesthood to reintroduce Keynes’ “continuing process of inflation” into the public’s mass psychosis as a “positive good” for everyone [a term made famous by John Calhoun when he claimed that slavery was just that]. But they know this claim is an outright lie, because as Hazlitt explains, inflation is a stealth global wealth tax that

is collected through lo$$ of purchasing power from those who hold their wealth in the form of Labor [for wage$] or Saving$ [in the common currency] and

is distributed through price increase$ to those who hold their wealth in the form of Real Assets or Borrowing$ [in the common currency].

The elites’ great high priest, Fed Chairman Powell, has even been so bold as to declare that as [no longer when] this positively good inflation comes “we're not going back to the same economy”. And, thus far at least, the mass psychosis is holding and the majority of Americans are actually baa-ing for “more stimulus/inflation” … like sheep for their own slaughter … as we noted in the PS to our last Candor article on the minimum wage.

For, you see, the easily distracted people of the Republic have never learned the immutable relationship between ecology and economy or the fundamental lesson of economics which Hazlitt so eloquently set forth above. And so they will never understand what Hazlitt called The Mirage of Inflation until it has swallowed them whole.

The people are lost in this mass psychosis from which any return to rationality now appears unlikely, because, as both Keynes and Hazlitt predicted, even the honest economists [and there are a few], when pressed, will equivocate [humbly or not] and misdiagnose, because the symptomatic unfolding of monetary inflation is factually subtle and circumstantially complex.

“The [continuing process of inflation] engages all the hidden forces of economic law on the side of destruction, and does it in a manner which not one [economist] in a million is able to diagnose.” Keynes, 1920

“Inflation itself is a form of taxation. It is perhaps the worst possible form, which usually bears hardest on those least able to pay. … It encourages squandering, gambling, reckless waste of all kinds. It often makes it more profitable to speculate than to produce. It tears apart the whole fabric of stable economic relationships. Its inexcusable injustices drive men toward desperate remedies. It plants the seeds of fascism and communism. It leads men to demand totalitarian controls. It ends invariably in bitter disillusion and collapse.” Hazlitt, 1946

But even so, as John Nash observed, what hard evidence there is [both historically and concurrently] of inflation violating “the limits on a person’s relation to the cosmos” … even if coherently presented by honest economists … could not alone dispel the deepening psychosis that controls a majority of the American public [as Hayek observed of the German people under the spell of national socialism even as their circumstances deteriorated].

The hard evidence against the sociopaths

Nevertheless, I offer the following as proof beyond a reasonable doubt [the evidentiary standard in this public criminal trial of the sociopaths] that inflation is already advanced and bearing down with increasingly dire consequences for the entire planet.

The price of gold indicates that the purchasing power of the US$ has decrease by 98% since 1971 when Nixon reneged on the Bretton Woods Agreement resulting in the slow collapse of the middle class' key societal roles as the economic SAVER$ and thus political RULER$ of the nation.

The elites conspire using central bank fiat credit to manipulate precious metal prices to blunt this reminder to the Republic of the extent of their robbery.

The elite’s [and their economists’] “official” inflation statistics are nothing less than “1984 doublespeak from the Ministry of Truth” designed to under-report inflation … as repeatedly demonstrated by “healthy skeptics” like John Williams' "Shadow Stats" and Wolf Richter’s “Wolfstreet” … by redefining some prices and excluding others altogether.

Using “rent” instead of housing “prices” is just one example of the manipulation, since “rent” tends to follow “mortgage payments” which can be suppressed using manipulated fiat interest rates while actual housing prices soar.

The inflation we experienced domestically in the 1970’s was subsequently and criminally exported [a form of toxic American financial waste dumping] to and absorbed by the innocent productivity of the working poor of the world [from Japan to VietNam] via the US$ as a global reserve currency through our massive consumption of imports and continuing trade deficits.

But this too will pass … resulting in the sudden collapse of the US$ as the world successfully rebels against this cruel US financial imperialism. And when that happens, living Americans will be forced to reap what past Americans recklessly sowed globally. We are seeing the rapid unfolding of this rebellion with numerous private and public digital, global currencies like BitCoin and the Russian and Chinese digital currencies attempting to flee what everyone knows is a counterfeit US$.

The inflation “tax” effecting a global wealth transfer [predicted by both Keynes and Hazlitt] is well documented and unprecedented. And while inequality of wealth is part of any virtuous economic system, this systemic inequality is sociologically unjust and must “reshape” the economic system we have known [where the word “tax” is a Greek word which simple means “to shape or form”].

[And if you will stop to think about it, it is arguably just that inflationism should lead to socialism, because the “wealth” it produces was extracted - via the inflation tax - from the public which should thus be entitled to enjoy it in common.]

And finally, for those who can manage to step outside their personal e-bubble, the planet itself … nature herself [to make it personal] … is more and more clearly struggling [and failing] to absorb the toxic waste from our increasingly frequent bouts of financial stimulation [a phrase suitable for public use instead of one that is more anatomically descriptive].

And when her absorption of our environmental rapine finally ends … which it will [first gradually then suddenly] … the full effect of the massively inflated costs we are currently externalizing into the environment and then ignoring in our “economic” accounting for inflation will finally become as hideously obvious to us as they already are

to the climate [in turmoil],

to the wild world [in mass extinction],

to our own progeny [in the growing intergenerational judgment that justice demands] and, if you can believe it,

to God [Rev 18] who, we are told, will declare “the time has come to destroy those who are destroying the earth” [Rev 11:18].

I rest my case … and leave the verdict to YOU the jury.

Bob Love

PS. Making the curse work backwards

“Come now, you who are rich, weep and wail over the misery to come upon you. Your riches have rotted and moths have eaten your clothes. Your gold and silver are corroded. Their corrosion will testify against you and consume your flesh like fire. You have hoarded treasure in the last days. Look, the wages you withheld from the workmen who mowed your fields are crying out against you. The cries of the harvesters have reached the ears of the Lord of Hosts. You have lived on earth in luxury and self-indulgence. You have fattened your hearts in the day of slaughter. You have condemned and murdered the righteous, who did not resist you.”

—James 5:5-6

Exposing and convicting the sociopaths in our midst is only the first step in our repentance. Once the psychosis is broken, we must “do” something and that requires intelligence.

So I leave the reader with a challenge to consider his/her moral obligation to be intelligent … and to ask why money arose after property and markets which were already advancing man’s material welfare within the limits of nature by facilitating a continuous, dynamic and just redistribution of the products of human labor and tools applied to the planet’s natural resources.

This pre-money arrangement is summarized in a fundamental equation which unites natural ecology and human economy:

Man’s Material Well-being = Natural Resources + (Labor * Tools)

But once money is added and then “financially” detached from all natural resources [ie. made fiat], money loses its natural and limited reason for existing at all and the fundamental equation begins to function as an unnatural, unlimited psychotic curse ... which the Federal Reserve now promotes as “the wealth effect”.

If this psychotic curse is to be broken, it will be because [as Aslan explained to Lucy and Susan at the StoneTable] "there is a magic deeper still which [finance does] not know ... that when a willing victim who has committed no treachery is killed in a traitor's stead ... Death itself will start working backward." And as James noted above, many willing and innocent laborers have already been slaughtered by the financial traitors and the number continues to grow. So we can start the curse working backwards … but only by taking the FIRST step of restoring our money’s hard link to nature’s resources as proposed above.

This restoration will almost immediately demand that we take a SECOND step backwards … and reconsider property which came after natural resources but before money. In that spirit, I encourage Candor’s readers to ponder [as did Adam Smith and others] John Locke’s 1690 Second Treatise of Government, Chapter 5: Of Property which speaks of divine purpose, of humanity, of natural resources and of property … both before and after money. It contains a true wealth of worthy ideas [including a description of real savings] which, if thoughtfully heeded, will certainly help us continue to unwind the psychotic financial curse gripping us today.

“[M]en come to have a property in several parts of that which God gave to mankind in common, and that without any express compact of all the commoners. ... As much as any one can make use of to any advantage of life before it spoils, so much he may by his labour fix a property in: whatever is beyond this, is more than his share, and belongs to others. Nothing was made by God for man to spoil or destroy. And thus, considering the plenty of natural provisions there was a long time in the world, and the few spenders; and to how small a part of that provision the industry of one man could extend itself, and ingross it to the prejudice of others; especially keeping within the bounds, set by reason, of what might serve for his use; there could be then little room for quarrels or contentions about property so established. ...

“This is certain, that in the beginning, before the desire of having more than man needed had altered the intrinsic value of things, which depends only on their usefulness to the life of man; or had agreed, that a little piece of yellow metal, which would keep without wasting or decay, should be worth a great piece of flesh, or a whole heap of corn; though men had a right to appropriate, by their labour, each one of himself, as much of the things of nature, as he could use: yet this could not be much, nor to the prejudice of others, where the same plenty was still left to those who would use the same industry. …

[For] the greatest part of things really useful to the life of man, and such as the necessity of subsisting made the first commoners of the world look after, as it doth the Americans now, are generally things of short duration; such as, if they are not consumed by use, will decay and perish of themselves: gold, silver and diamonds, are things that fancy or agreement hath put the value on, more than real use, and the necessary support of life. ... And thus came in the use of money, some lasting thing that men might keep without spoiling, and that by mutual consent men would take in exchange for the truly useful, but perishable supports of life.

Thus in the beginning all the world was America, and more so than that is now; for no such thing as money was any where known. Find out something that hath the use and value of money amongst his neighbours, you shall see the same man will begin presently to enlarge his possessions. ... But since gold and silver, being little useful to the life of man in proportion to food, raiment, and carriage, has its value only from the consent of men, whereof labour yet makes, in great part, the measure, it is plain, that men have agreed to a disproportionate and unequal possession of the earth, they having, by a tacit and voluntary consent, found out, a way how a man may fairly possess more land than he himself can use the product of, by receiving in exchange for the overplus gold and silver, which may be hoarded up without injury to any one [real savings]; these metals not spoiling or decaying in the hands of the possessor. This partage of things in an inequality of private possessions, men have made practicable out of the bounds of society, and without compact, only by putting a value on gold and silver, and tacitly agreeing in the use of money: for in governments, the laws regulate the right of property, and the possession of land is determined by positive constitutions.

Locke explains things from “the beginning” forward. If he is correct, perhaps, the forces of movement forward to a “just commonwealth” from “free markets” has already begun … bringing us “back” to where we began in many ways. If true, the inflation psychosis may just be the catalyst for a new revolution. Think about it.